Triangulation in finance refers to the exploitation of price discrepancies in different markets to generate risk-free profit. It’s a sophisticated arbitrage strategy that typically involves three or more currencies, assets, or even markets, creating a loop where an initial investment is converted through various exchanges, ultimately returning a larger sum than the original. The core concept relies on market inefficiencies, temporary misalignments in pricing that a skilled trader can identify and capitalize on. The classic example is currency triangulation. Imagine the EUR/USD exchange rate is 1.10, the GBP/USD rate is 1.30, and the EUR/GBP rate is quoted as 0.80. This presents an arbitrage opportunity. A trader could start with Euros, convert them to USD, then convert the USD to GBP, and finally convert the GBP back to Euros. Here’s how it works: 1. **Start with EUR:** Let’s say you begin with €1,000,000. 2. **Convert to USD:** At EUR/USD 1.10, you receive $1,100,000. 3. **Convert to GBP:** At GBP/USD 1.30, you receive £846,153.85 ($1,100,000 / 1.30). 4. **Convert back to EUR:** At EUR/GBP 0.80, you receive €1,057,692.31 (£846,153.85 / 0.80). By completing this loop, you’ve made a risk-free profit of €57,692.31, assuming transaction costs are negligible. While currency triangulation is a common illustration, the principle applies to various financial instruments. It could involve different stock exchanges, commodity markets, or even debt instruments. The key is identifying a situation where the implied relationship between the assets doesn’t align with the actual market prices. However, successful triangulation is challenging. Several factors can quickly erode potential profits: * **Transaction Costs:** Brokerage fees, exchange fees, and other trading costs can significantly reduce or eliminate profits. * **Speed of Execution:** Market prices change rapidly. By the time a trader identifies an opportunity and executes the trades, the price discrepancy may have disappeared. High-frequency trading (HFT) firms are particularly adept at exploiting these fleeting opportunities. * **Market Liquidity:** Insufficient liquidity in any of the markets involved can make it difficult to execute large trades at the desired prices. * **Exchange Rate Fluctuations:** Exchange rates can move significantly during the execution process, rendering the arbitrage opportunity unprofitable. * **Regulatory Constraints:** Some markets have regulations that restrict or prohibit certain types of arbitrage trading. Despite these challenges, triangulation remains a viable strategy for sophisticated traders with access to advanced technology, real-time market data, and efficient execution platforms. While perfect risk-free arbitrage opportunities are rare in today’s interconnected markets, the pursuit of triangulation helps to keep markets efficient by correcting pricing discrepancies. In essence, by exploiting these temporary misalignments, traders contribute to the overall price discovery process and market equilibrium.

486×302 global finance triangulation technocratic tyranny from thetechnocratictyranny.com

486×302 global finance triangulation technocratic tyranny from thetechnocratictyranny.com  1000×636 triangulation sight size from www.sightsize.com

1000×636 triangulation sight size from www.sightsize.com  850×1202 triangulation approaches finance research from www.researchgate.net

850×1202 triangulation approaches finance research from www.researchgate.net  1024×768 triangulation from www.slideshare.net

1024×768 triangulation from www.slideshare.net  474×355 triangulation approach valuation delivers price ipcg from www.ipcg.com

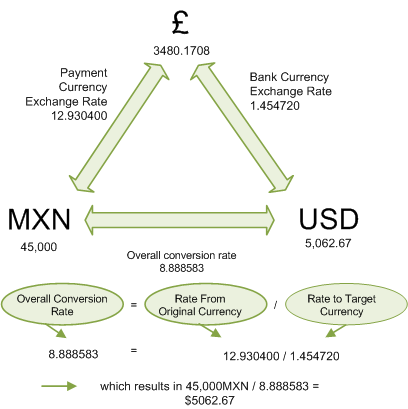

474×355 triangulation approach valuation delivers price ipcg from www.ipcg.com  408×409 triangulation currencies from support.sage.co.uk

408×409 triangulation currencies from support.sage.co.uk  1157×688 currency triangulation from desktophelp.sage.co.uk

1157×688 currency triangulation from desktophelp.sage.co.uk  660×469 triangulation raise probability making good decisions from medium.com

660×469 triangulation raise probability making good decisions from medium.com