“`html

Understanding PPP Finance Structures

Public-Private Partnerships (PPPs) are collaborative ventures between government entities and private sector companies, typically for infrastructure projects. Financing these complex undertakings requires sophisticated structures that distribute risks and rewards appropriately. Several key finance structures are commonly employed in PPPs. Project Finance: This is the cornerstone of many PPPs. It focuses on financing the project itself, independent of the balance sheets of the sponsoring organizations. Debt is secured primarily by the project’s future cash flows, meaning lenders assume a significant portion of the project’s risk. A special purpose vehicle (SPV) is usually created to manage the project and isolate it from the financial troubles of the parent companies. The SPV enters into long-term contracts for construction, operation, and maintenance. Lenders scrutinize these contracts to ensure the project’s revenue streams are reliable. Equity Contributions: Private sector participants invest equity into the SPV, providing crucial upfront capital and demonstrating commitment. The amount of equity required varies depending on the project’s risk profile, the availability of debt financing, and regulatory requirements. Higher-risk projects typically demand more equity. Equity investors expect a return commensurate with the risk they undertake, which often comes in the form of dividends from project profits. Debt Financing: A significant portion of PPP financing comes from debt, usually in the form of bank loans, bonds, or a combination of both. Debt can be structured in various ways to suit the project’s needs. Senior debt holds priority in repayment, while subordinated debt carries higher risk but also potentially higher returns. Debt tenors are often long-term to match the project’s lifespan and cash flow projections. Government guarantees or partial risk guarantees can sometimes be used to attract lenders and lower borrowing costs. Government Contributions: Governments often contribute to PPP projects through various mechanisms. This can include direct capital grants, availability payments (where the government pays the SPV for the availability of the infrastructure), shadow tolls (payments based on usage), or revenue sharing. These contributions can enhance the project’s financial viability and attract private investment. The structure and amount of government contribution are crucial for balancing risk and reward between the public and private sectors. Risk Allocation: A critical aspect of PPP finance is allocating risks appropriately between the public and private partners. Construction risk (e.g., cost overruns, delays) is usually borne by the private sector, as they are better equipped to manage it. Demand risk (e.g., lower-than-expected usage) can be shared, assumed entirely by the private sector, or partially mitigated through government guarantees. Force majeure risks (e.g., natural disasters) are typically addressed through insurance or shared between parties. Financial Modeling: Robust financial models are essential for assessing the viability of PPP projects. These models project future cash flows, calculate key financial metrics (e.g., internal rate of return, net present value), and perform sensitivity analyses to understand the impact of various risks. Lenders and equity investors rely heavily on these models to make informed investment decisions. The models must be transparent, accurate, and regularly updated to reflect changing circumstances. PPP finance structures are complex and require careful planning, negotiation, and legal expertise. The goal is to create a structure that attracts private investment, delivers public benefits, and allocates risks fairly between the public and private sectors, ensuring the long-term success of the project. “`

356×418 private finance ppp project financed money from ppp-certification.com

356×418 private finance ppp project financed money from ppp-certification.com  638×479 mena project ppp finance from www.slideshare.net

638×479 mena project ppp finance from www.slideshare.net  1800×846 ppp big picture from ritholtz.com

1800×846 ppp big picture from ritholtz.com  688×754 introduction basic ppp project structure apmg public from ppp-certification.com

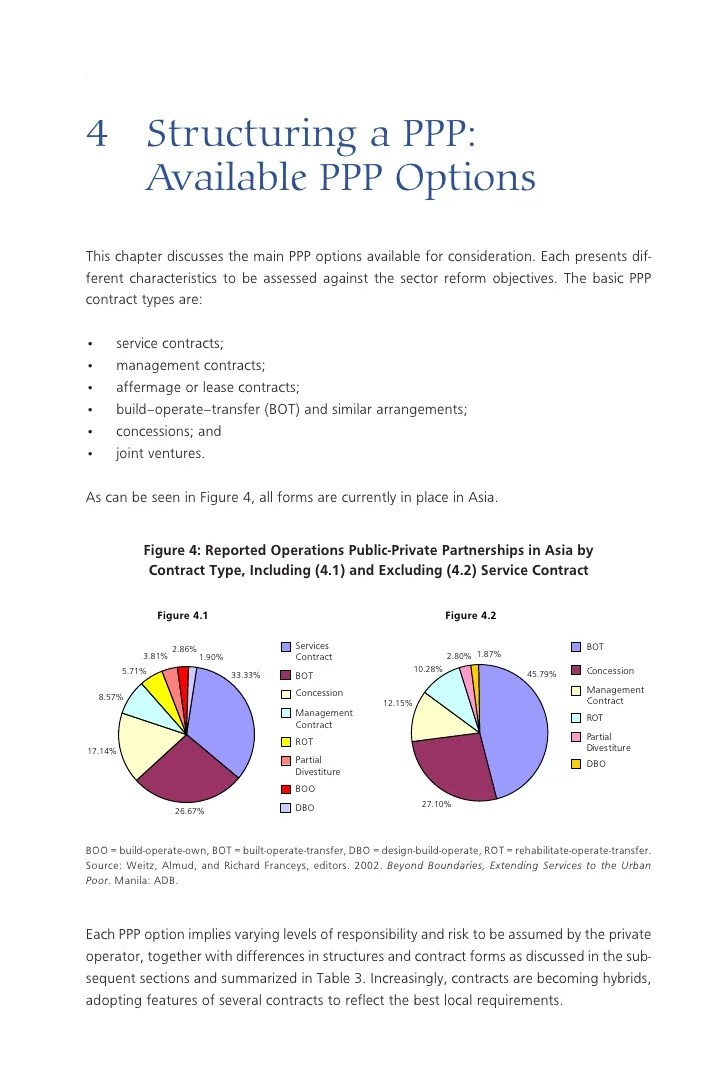

688×754 introduction basic ppp project structure apmg public from ppp-certification.com  728×1092 chapter structuring ppp ppp options from www.slideshare.net

728×1092 chapter structuring ppp ppp options from www.slideshare.net  1280×720 ppp public private partnerships explained from financialmodellingpodcast.com

1280×720 ppp public private partnerships explained from financialmodellingpodcast.com  448×448 typical ppp structure source akintoye scientific diagram from www.researchgate.net

448×448 typical ppp structure source akintoye scientific diagram from www.researchgate.net  1282×636 risk management ppp projects mpg from mahanakornpartners.com

1282×636 risk management ppp projects mpg from mahanakornpartners.com  716×417 typical structure ppp project scientific diagram from www.researchgate.net

716×417 typical structure ppp project scientific diagram from www.researchgate.net  850×521 leveraging defi fund major public infrastructure projects ledger from ledgerinsights.com

850×521 leveraging defi fund major public infrastructure projects ledger from ledgerinsights.com